Fifteen years of owning Apple, Jim Cramer’s assistant, lock-in are all the same topic

Meet me right now for this week’s Live Q&A Chat in the Trading With Cody Chat Room or just email me your question. Here’s today’s report in to get you in the mood.

An old friend of mine who used to be Jim Cramer’s research assistant fifteen years ago, emailed me out of the blue today with a very nice note that happens to be quite relevant to Trading With Cody subscribers today too:

Will Gabrielski May 2, 2018, 9:55 AM to Cody

Cody, since you are the man who called aapl before anyone even had a nano….I was bragging about that to a friend, was wondering if you had a link or copy of one of your original pieces on the “locked in” aapl effect.

So I did a quick search on the Internet for some of my old analysis about Apple from more than a decade ago. With Apple reporting quarterly revenues of $61.1 billion and quarterly earnings of $2.73 earnings of last night — and with Apple still being my single largest position as it has pretty much for most of the last fifteen years since I first invested in AAPL when the stock was at a split-adjusted $1 per share — I think you’d find this analysis from 2004 and from 2007 to be a fascinating reminder yet again of why it’s so important to focus on finding great Revolution Investing opportunities (including Google at $45 or Facebook at $25 or Nvidia at $30 or Axogen at $4 and so on) and looking out over a decade or more.

Notice that in this first report I found that I wrote on The Street back in 2004(!) that Apple has increased its sales 30-fold and its earnings 130-fold since that second quarter 2004 earnings report I highlighted in there. Yes, earnings at Apple have gone up 130-fold since I first bought the stock — and guess what! The stock itself, AAPL, has gone up 60-fold since that article was published when the stock was at a split-adjusted less than $3 per share (Apple is indeed up 170-fold since I first bought it it at a split-adjusted $1 per share cost basis back in March 2003). So anyway, read the whole article because it also outlines some of the same Revolution Investing principles I use every day to find our latest and our next stock picks.

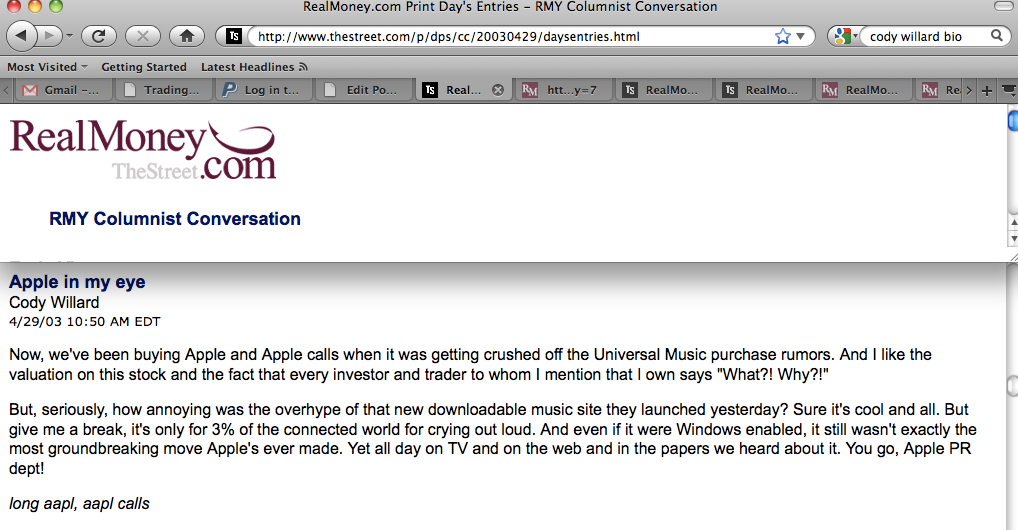

Apple Should Offer Shiny Quarter by Cody Willard

Oct 13, 2004

I want to walk through what I expect to see when Apple ( AAPL) reports its quarterly earnings tonight. It only seems right, given my oft-stated affection for the company’s products, that I walk through my vision for Apple’s report.

The sell-siders expect the company to report earnings of 18 cents on sales of $2.15 billion tonight. I think the company will blow those numbers out of the water.We all know that they’re selling every iPod they can make. Little kids, teenage girls, parents, bachelors, early tech adopters — everyone wants an iPod. The sell-siders have slowly but surely been coming to terms with that fact, and have been ratcheting up their iPod estimates like mad.

Just last week, one sell-sider raised his already “aggressive” estimates for iPod sales in 2005 from 8 million to 10 million. Ten million units next year! This is a an entire industry that essentially didn’t even exist two years ago. Likewise, I think the company is taking (or beginning to take) serious market share back from Microsoft.Understand that when you only own 3% of the market, simply taking another 1% is a 33% jump — even if there’s no growth in the overall market. That’s what Apple is finally doing. And it’s in large part due to the runaway success of the iPod.

Anecdotally, last night I got a call from a PR person at Apple who was very gracious in offering to send me a temporary iMac to play with until I receive my own. I’ve got the spot in my apartment all arranged and ready to hang this iMac on the wall for jamming purposes, but putting a temporary iMac on my office desk next to my other computers isn’t what I’m looking to do.

I asked the very nice lady if, rather than sending me a temp, there was any way she could just speed up the delivery of my own model. Alas, she said there was no way because they just can’t meet demand for the new iMacs. People (like me) are returning to the Macintosh platform because we’ve fallen in love with Apple all over again from our warm and fuzzy experiences with iPod and iTunes. (Of course, my iTunes doesn’t sense that I’ve got an Airport Express connected to my stereo, so I still can’t wireless stream my music, but that’s another story.)

For next quarter, the sell-siders expect Apple to report earnings of 28 cents (Cody note from real-time 2018, 28 cents back then is equal to a split adjusted 2 cents today!) on $2.52 billion of sales. I think that’s a very low hurdle for the company to raise, as the iPod will be in every affluent family’s stockings and under every other family’s Christmas tree that can possibly scratch together the money. Likewise, the Apple computers are going to have a great Christmas season, finally, after years of threatening and disappointing, taking more market share from the WinTel monopoly.

I bought some Apple calls today to add to the Apple common stock that I’ve held since exercising Apple calls so many moons ago. I know dozens of hedge fund friends who are short this thing because “the valuation’s too high” or because “the faceplate on the iPod scratches too easily and there’s too much competition coming” or because “Microsoft is going to do to Apple in this MP3 business what they did to them in the PC business.”Perhaps they’re right. Perhaps they’ll be right in the long term. But I think the odds are that Apple reports a stellar quarter and raises guidance. I think the stock moves higher, and I placed my bets accordingly.

Okay, Cody back in real-time 2018 now. Here’s another report I wrote about Apple, this one from the Financial Times in 2007 when Apple was trading at a split-adjusted $12 per share:

Embrace the ‘revolutionomics’ of the internet by Cody Willard

FEBRUARY 2, 2007

The endgame of the internet is the total empowerment of the end user. Because the internet has been built on open standards and the free flow of information, the 1.5bn people on this planet who have access to the web will continuously move to the places on the net that empower and liberate them the most. We users will constantly (and at an accelerated pace) move away from centres of control and toward self-empowerment.

And just as the tendency towards disorder in the universe cannot be controlled, nobody can stop the virtuous entropy of the internet revolution. I have coined the term “revolutionomics” to describe this dynamic. “Lock in”, “switching costs” and many other similar strategies that the world’s leading technology companies have built their business models on have no place in the end-user-powered networked world.

Tech companies have long tried to lock their customers into proprietary standards, thus creating high switching costs for them. Control was yesterday’s business model. The model that increasingly works on the internet is to empower customers rather than control them.

Edward George Bulwer-Lytton, the English novelist and playwright, once wrote that the pen is mightier than the sword. That the internet revolution will be fought using words, software and open networks – and on such a massive scale – is precisely why its impact will be much bigger than any revolution this world has gone through. Every revolution that has succeeded in the long term, including the American Revolution, has been about shifting power away from central control. As the costs for technology development in this networked future continue to collapse, the only differentiator becomes one of execution and strategy.

Only those companies that design their systems from the ground up to empower the end-user have any chance of long-term success. Look no further than what is going on in the media industry for what happens to those who fight the virtuous entropy. Google, the fastest- growing company in the history of capitalism, and a stock that I have owned since it went public, focused on establishing itself as a de facto conduit for the world’s content for the first few years of its existence.

As its reputation for openness and empowerment of the end-user has grown, Google has reaped big rewards: its market capitalisation is more than $150bn. No company has embraced the revolutionomic model as Google has. Others, such as Yahoo, Microsoft, Sun and Apple, still obsess with making sure you are locked into their systems. Want to forward your Yahoo mail to another account? Upgrade for $19.99 a year and Yahoo will “empower” you. Gmail empowers you to do that for free from the start.

The only thing Yahoo accomplishes in this model is to alienate its user base as the hundreds of millions of Yahoo mail users shift to alternative and empowering e-mail systems such as Gmail. In the process, Google makes lots of money selling advertisements as you retrieve your e-mail, making up for the revenue it forgoes by not charging users directly as Yahoo does. That is virtuous entropy in motion.

Want to listen to music you purchased from Apple on another MP3 player? Sorry, Apple and the music labels think it is more important to empower themselves than the end user. And people wonder why music sales are down double digits over the past few years. Hey labels, wake up and start monetising peer-to-peer and all other forms of open music distribution.

Sure enough – though it took a full decade after MP3 file trading first became mainstream – the music labels have begun to license the selling of open-standard MP3 songs on MySpace.com and elsewhere on the internet. Anybody want to bet that we see music sales climb in 2007? It turns out people will pay for a good product delivered to them simply and in a form they can use on any system.

Years ago I trademarked the term “they can’t stop the revolution” as a catchphrase for the virtuous entropy of revolutionomics. And, indeed, that is exactly the point. Neither Yahoo, nor Apple, nor the music labels, nor the film studios can stop the empowerment of the individual.

Within the next few months, television and film studios will follow in the record labels’ footsteps as they, too, recognise that it is easy and profitable to monetise the empowerment of their end users. The content owners that have been fighting the revolution, including Disney and Warner Music Group, are, ironically enough, perfectly positioned for a golden age of profitability as their end-users have ever more access to the content on ever more devices. And the virtuous monetisation of distributing that content begins.

Cody in real-time 2018. Turns out Google isn’t nearly as open these days as it used to be and it sure does use a lot of lock-in to keep people in its eco-system of Google, Gmail, Android, Nest, etc, etc. And Apple, of course, has really mastered its lock-in approach.

Meanwhile, monetization and distribution of content are still two wars being fought, aren’t they? And where there’s wars, there’s Revolution. And where there’s Revolutions, there are Revolution Investment opportunities. Let’s keep focused on what matters — like finding the next Apple at $1 per share, right? Okay, okay, no promises. But I’ll keep using many of these same principles that we’ve learned and profited so much from over the years to try my best!

{kind=link}