Markets Outlook: Reflexivity, Blow-Off Tops, And Other Horror Stories

I don’t know when the ongoing Blow-Off Top Of The Bubble-Blowing Bull Market™ that we’ve been riding for the last 12 years will end. And maybe after ten plus years of me being long and strong and having diamond hands without even knowing that term existed, maybe I’m wrong to turn more cautious thinking that we are currently in the throes of the top of a bubble anyway. Maybe the economy will reopen and rejuvenate in such a strong manner that corporate earnings in 2022 and 2023 are going to be so strong across the board that today’s current batch of valuations are actually going to be remembered as bargains. I simply don’t think that’s the most likely outcome here.

And if I’m right that we’re in the throes of the Blow-Off Top Of The Bubble-Blowing Bull Market™, I do not want to be overly long and on the wrong side of the Great Unwind when it does start. Again, I’m not calling for a near-term crash, but I am saying that it’s likely going to be hard for the bulls to make as much money this year as they did last year.

Look, trading and investing is tough and it’s not meant to be fun. There’s always someone on the other side of every trade you make — always think about who that is and why they are willing to take the other side of your transaction. When you buy, why are they selling it to you at that price? When you sell, who is buying it from you and what are their motivations? Remember, I’ve talked before about how Good Analysis Starts With Empathy.

Well, so let’s answer this question right now. Who is buying stocks and cryptos from me when I’m trimming and selling for the last month or so? Sure, there are banks and institutions and hedge funds and family offices investing and trading just as always. On the other hand, remember two years ago when I got back from a hedge fund investment conference in Abu Dhabi and everybody was desperate for returns:

“While I’ve talked about how artificially low (including negative) interest rates have forced savers around the world further out on the risk curve many times, it was hearing the many managers of pensions and sovereign wealth funds and family offices talking about how they are investing in alternative assets and ideas to try to get better returns that drove home that trend…

…Interestingly, I was one of very few traditional long/short equity hedge funds that I met in Abu Dhabi. Most of the hedge fund managers we met were running hundreds of millions or billions of dollars trading derivatives or credit spreads or currencies and so on, and most of the major funds were also looking for those kinds of investments. Of course, the lack of focus on traditional stocks and funds that invest in publicly-traded stocks makes me think that there is probably more opportunity in such assets than people realize. I certainly see some very compelling long ideas in Revolutionary companies like WORK and TWTR and TSLA”

Since that post, back a year and a half ago, WORK went from $21 to being bought out at $45, TWTR went from $27 to $61 and TSLA went from $81 to $616…and most of those funds that were looking everywhere but in the stock market for big gains are…well, pretty much in the markets now and long a bunch of stocks and even long a few cryptos now.

And now that those stocks and the cryptos and most other assets have gone parabolic in the last year coming on top of the ten year bull market you and I were riding together before they were in on the fun, well, the billion dollar fund managers are joined by 23 year-old Tik Tok influencers doing bitcoin trading astrology. Yes, for real, and she’s very popular according to the NY Post, and she’s even been right about some of bitcoin’s action in the last few months! If you’re selling cryptos and fintech stocks right now, you’re selling to her and her followers and my friend’s son who just graduated from a rural tiny school and who’s unemployed uncle gave $500 to “Buy some cryptos. And make sure you get some fintech. I don’t know the symbol, but just look it up and you’ll do fine over the long-run.” Bearish anecdotes everywhere I look, as I wrote recently.

The other thing to remember about who’s on the other side of your trade is always to remember that there are smart, cutthroat traders and investors who went to the best schools and have access to more research and real-time data and instant trading access to all kinds of derivatives to layer into their bets…and the only thing they do all day every day is figure out how to take your money out of your pocket in mostly legal ways. They’re not playing around. They have no sympathy for you, even if they might empathize with you to better understand your motivations to better take your money.

Mr. Market is mean. He’s not nice. He can be cruel. He can force liquidations that create other liquidations. He can shut off access to capital. He can take down 200 year-old banks in a day. In one day.

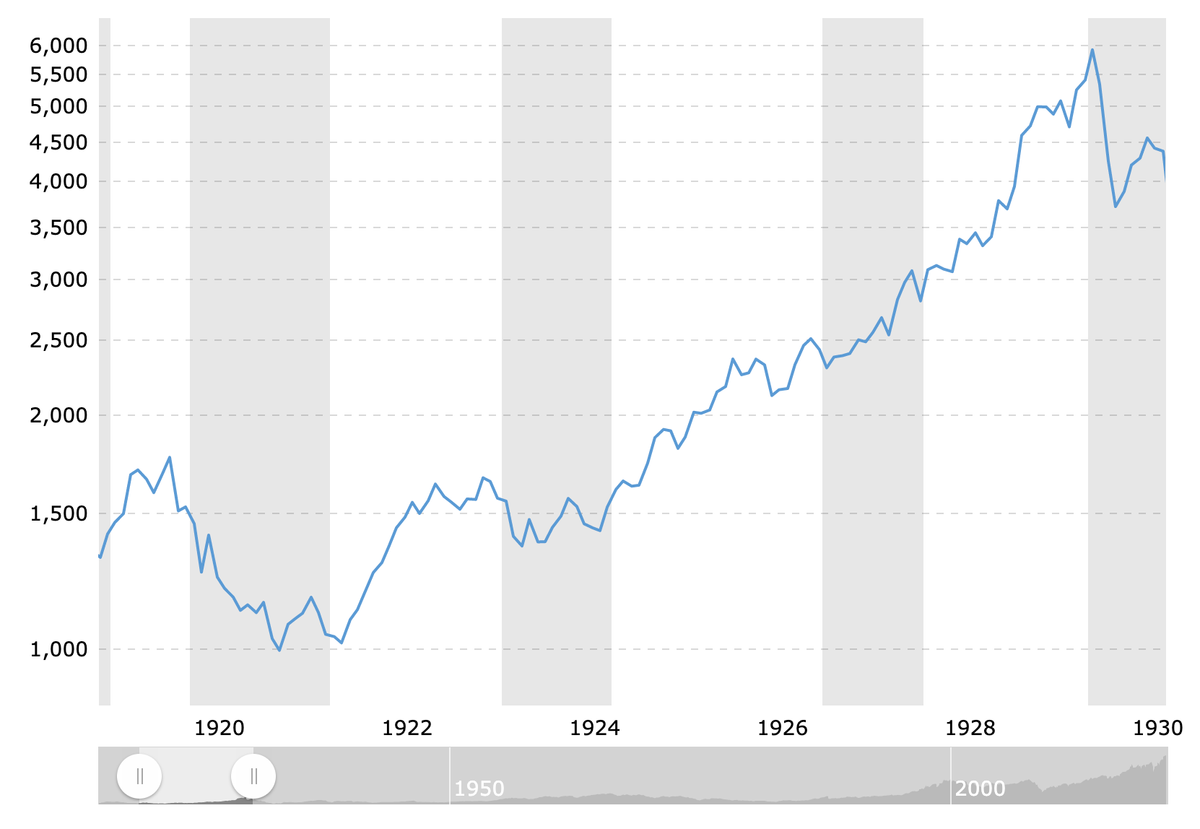

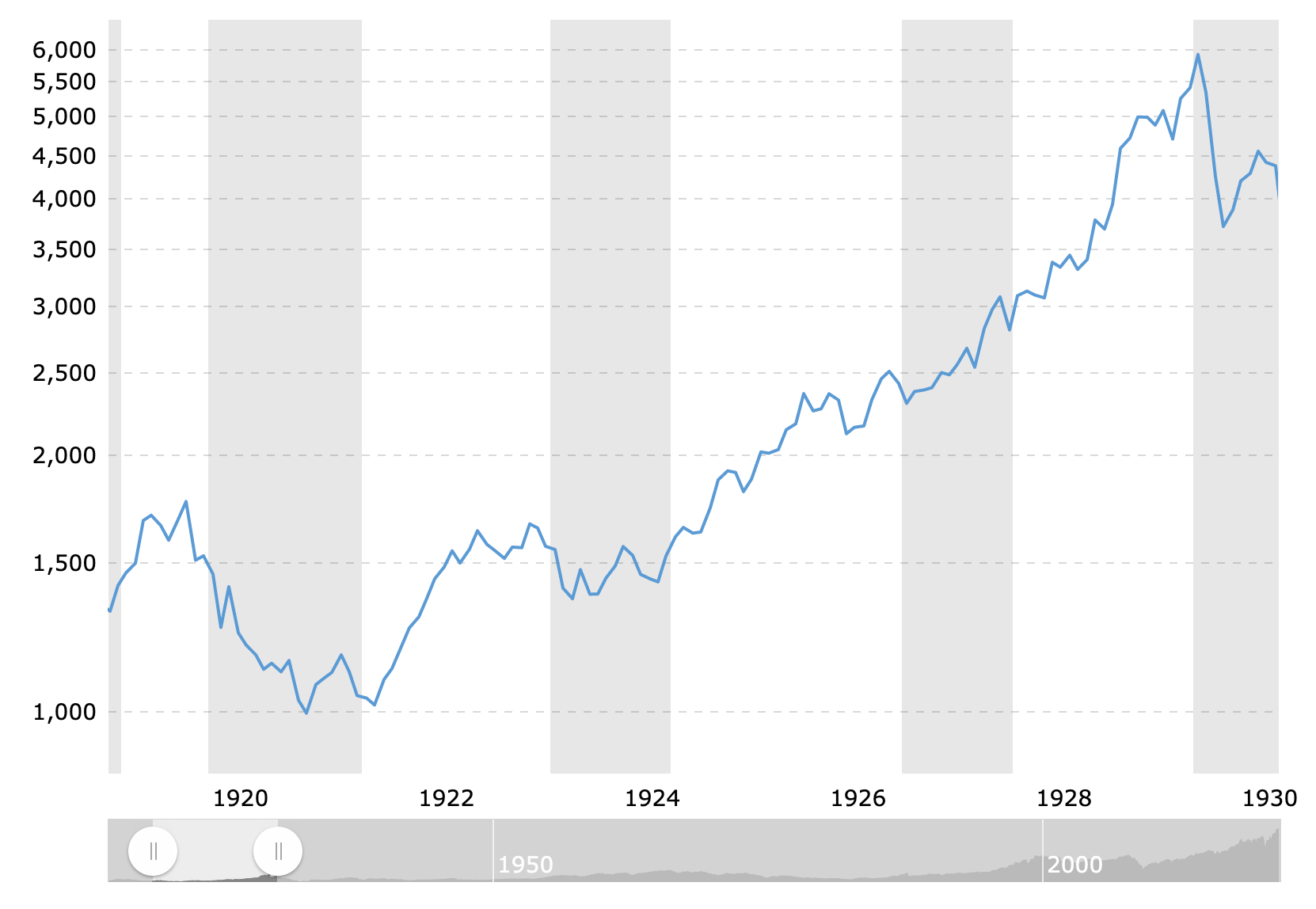

Sometimes the markets lead the economy and not the other way around. Ironically, when we were young, we were taught that the Great Depression started when the stock market crashed on Black Friday in 1929. But then when we get older into high school and college, we’re taught that it wasn’t actually the crash that created the Great Depression, rather the economy was already crashing and the stock market just didn’t realize it as it continued on its merry way toward a terrible Blow-Off Top of a nine-year Bubble-Blowing Bull Market that culminated with the DJIA up 400% from the 1921 lows to the 1929 highs.

But looking back, it’s clear that both theories are equally right and wrong — the market crashed because the economy wasn’t as good as the market thought it was AND the economy crashed because the markets shut down access to capital for investment and growth. It was reflexive to borrow the great hedge fund manager, George Soros, term (bold is mine).

“I continued to consider myself a failed philosopher. All this changed as a result of the financial crisis of 2008. My conceptual framework enabled me both to anticipate the crisis and to deal with it when it finally struck…

I can state the core idea in two relatively simple propositions. One is that in situations that have thinking participants, the participants’ view of the world is always partial and distorted. That is the principle of fallibility. The other is that these distorted views can influence the situation to which they relate because false views lead to inappropriate actions. That is the principle of reflexivity…

Recognizing reflexivity has been sacrificed to the vain pursuit of certainty in human affairs, most notably in economics, and yet, uncertainty is the key feature of human affairs. Economic theory is built on the concept of equilibrium, and that concept is in direct contradiction with the concept of reflexivity…

A positive feedback process is self-reinforcing. It cannot go on forever because eventually the participants’ views would become so far removed from objective reality that the participants would have to recognize them as unrealistic. Nor can the iterative process occur without any change in the actual state of affairs, because it is in the nature of positive feedback that it reinforces whatever tendency prevails in the real world. Instead of equilibrium, we are faced with a dynamic disequilibrium or what may be described as far-from-equilibrium conditions. Usually in far-from-equilibrium situations the divergence between perceptions and reality leads to a climax which sets in motion a positive feedback process in the opposite direction. Such initially self-reinforcing but eventually self-defeating boom-bust processes or bubbles are characteristic of financial markets, but they can also be found in other spheres. There, I call them fertile fallacies—interpretations of reality that are distorted, yet produce results which reinforce the distortion.”

Far-from-equilibrium conditions was what we had in 2010-2013 when we loaded up on Revolutionary stocks and started buying cryptos like bitcoin. Far-from-equilibrium conditions might be what we have in front of us right now when I suggest getting cautious instead.

We don’t want to be a permabull (and as I’ve talked about a million times, you for sure don’t want to be a permabear!). We have to be flexible. We have to let your analysis and your risk/reward scenarios dictate how much risk we’re taking and when. We have to pay some attention to the cycles, the self-reinforcing cycles that drive economies and markets and valuations and earnings and societal interactions and bailouts and financial crises and bubbles and busts and, heaven forbid, just simple stagnation.

It’s like everybody forgets that markets can both bubble and crash and stagnate. They forget that markets can grind for years on end without making new highs, or without even making higher highs. Do you not remember telling your money manager sometime in 2010-2012 that “If I’d just handled the Great Financial Crisis (and/or the Dot Com Crash) a little better, I’d be in better shape.” I used to hear people say that to me all the time. I haven’t heard anybody say that lately. Everybody’s having fun in this market…at least for now.

Most traders will tell you that they are “just trading the market that is in front of them.” Well, I don’t know when the bubble will pop, but I do know that I don’t want to be on the wrong side of this market when it does. And I do know that we won’t know the bubble has really popped until the self-reinforcing reflexive feedback loop has made it painful for the vast majority of people who are right now feeling wealthy, feeling secure, feeling like they’ve got this trading and investing thing all figured out.

We are all fallible. Be careful while it’s fun. Be bold when it’s painful. That’s how I’ve done it for the last twenty five years. We were boldly buying these assets when it was painful for others. I’m careful right now because everybody else is having fun.

I spend a lot of time looking for new ideas and I won’t let my overall market outlook here deter me from buying a new name or two. But I want to remain overall cautious and less aggressive than I have been for most of the last decade. As a matter of fact, I might have at least a couple Trade Alerts that I’ll be sending out this week, one long and one short idea. Being flexible, see?