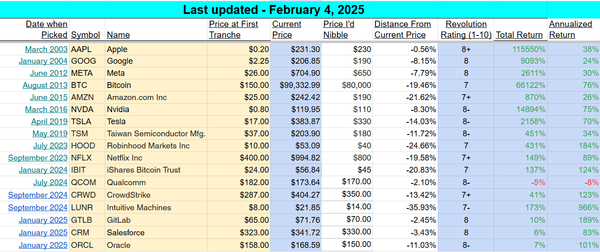

Portfolio run through

A decade ago, I was sitting in Jim Cramer’s offices down on Wall Street and we were talking about my dream of running my own hedge fund. Cramer had heard from the editor of TheStreet.com, where I’d been publishing investment articles for a couple years, that I wanted to launch a fund and he sat down with me several times to give me advice, contacts in the industry and insights into how it all worked. Love Jim or hate him, and if you’re in the markets, you probably do one or the other. One thing I have been real smart about throughout my career was to take the good lessons that you learn from anybody you work with and apply them to your own life, your own career, and/or your own approach to the markets.

And one of the best lessons I ever learned from Cramer was to run through your entire portfolio on a regular basis and to rate each stock on a scale from 1 to 10. 1 being “Close this position immediately” and 10 being “Make this position as big as possible as fast as possible”. I still do this with the TradingWithCody portfolio every week and it helps guide the weighting of each of the respective positions in my own portfolio, and when a stock’s rating falls to 6 or below, I will usually remove it from the portfolio entirely.

So let’s run through the portfolio from top to bottom, and discuss each position now that we’ve had lots of earnings report this season. I’m going to go in order from highest-rated stock to lowest.

Apple (9) – Apple reported a “disappointing” quarter, which means Apple “only” made $8.8 billion in net profit in the last three months. That’s almost $100 million in profit per day for the last three months. The company should make $50 billion in profits, not sales, but profits in the next 365 days, and the market cap is right now at $500 billion or so…plus they have $100 billion in net cash in the checking account and now we’re getting a good dividend yield to boot. The New iPhone is coming and it’s going to have even more new talk-able features than ever before.

Google (8) – Google reported a strong quarter and the company is apparently figuring out how to monetize mobile and YouTube, which means they’ve got two new viable revenue streams to grow.

Fusion-IO (9) That spending on capital infrastructure Facebook talked about on their call? I expect a healthy chunk to go FIO’s way. This is a VC investment for us, I’m looking to make 10x because that’s how big the addressable market and how far ahead of the competition FIO is. And if this were in your VC portfolio you wouldn’t think about the swings on the secondary market, so think of the stock that way, take advantage of any weakness to add to your position. FIO reports August 9th and I’m talking to all my sources right now, we’ll have more to discuss soon.

Facebook (8) As much as the stock market hated the call I’m still bullish on Facebook. They have a great team in place that is totally focused on growing the platform. Five years from now they’ll have big revenue streams from ecommerce, mobile ads, payments and content delivery. You want to own the name before any of that stuff gets off the ground.

Lindsay (8) LNN is booming and can barely keep up with orders, the American breadbasket is going through a drought like it hasn’t seen in half-a-century. From the Ozarks through the plains, water management has become absolutely crucial, and Lindsay’s products are making up an ever bigger percentage of farmers’ costs. And LNN’s inputs costs should actually go down over the next couple quarters while their pricing power increases. The stock has done well but is still under a billion dollar market cap and has plenty of room to run.

F5 (8) The earnings call on July 18th confirmed that management is executing. The service side of the business is exploding and their file virtualization business is finally starting to ramp up. Holding steady, F5 is an acquisition target for about six competing companies, and I think it could be the object of a bidding war.

Amazon (8) Know what season has started? Believe it or not the Christmas shopping season, retailers are gaming out how they’re going to attract you over the next two months. Amazon’s enormous base of customers, who already have they shipping address and credit card information saved on the site, are going to spend more than they ever have I expect this to be AMZN’s best holiday season by a big margin. I was happy with the earnings call, the capex number doesn’t bother me, it gives me confidence that Amazon is building out their fulfillment and shipping platform.

Baidu (8) Baidu is up about 10% since they reported and I think they are poised to move higher in the next few months and years. This is one of the few Chinese stocks that American fund managers can buy with the confidence that it’s not a fraud, so there should be some good flows into the name. Baidu is breaking into the ecommerce market in a big way, despite what the headlines say, and I’m getting reports from my sources on the ground that their JV with Rakuten might be getting some traction. Their outside strategic investments like in Qunar, a travel site, are paying off handsomely, which should add about 20% to revenues within the next three year.

DDD (8) Another blazing quarter and the company reiterated their full year guidance. I was worried about management rolling up 3D printing companies and boasting about the revenue but I actually really like the revenue mix they have right now, lots of recurring customers. And with every company out there struggling in Europe, DDD increased sales sequentially. Plus I love their booming healthcare business, that’s going to be bigger than anyone on the Street realizes yet.

Broadcom (8) Up about 8% from it’s quarterly report, Broadcom is hitting on all cylinders. Their 5G Wifi chip has the geeks drooling and Qualcomm terrified. There’s going to be a new whole world of apps built on low-power Bluetooth, of which Apple is the biggest proponent, so Broadcom is about to become ever more critical to the iphone ecosystem.

Juniper (8) Juniper is up nicely since they reported, about 11%. The analysts keep taking down their target prices as Verizon and AT&T cut back overall capex but JNPR’s should keep pulling down the spending that’s out there. Their newest router is finally attracting customers and I’ve been hearing from my sources that it’s becoming a must-have for IT departments.

Sandisk (7) This one’s rated a 7 since it’s up about 20% from the earnings call. SNDK will continue to execute and grow as the flash market grows but a lot of the upside has been realized, at least in the short term. As I’ve been saying for years SNDK’s products are such a critical piece of so many different ecosystems, don’t be surprised by a big bid out of nowhere for the whole company.

Nuance (7) Apple’s new iphone is going to lean heavily on Siri, especially now that it will have native turn-by-turn GPS. Nuance is almost like a patent play on voice recognition, if they haven’t developed it, they probably own the IP. At a market cap of $6.35 billion I’m not sure how much bigger it can get. Keeping it for now.

Shorts –

Apollo (8) Apollo is down another 25% on the month and the future looks truly bleak. Management sold a profitable U.K. business at exactly the wrong time, and bought a math-education software company to try and up-sell broke school districts. Looking at Apollo’s map of schools there are about a half dozen that I think could lose accreditation over the next five years, which would roughly slice revenues in half. And the Street is buzzing about David Einhorn possibly shorting the stock and if that becomes publicly known expect the name to crumble 15% on the day.

Dollar General (8) Not one of my hedge fund friends like this short, which makes me love it even more. Retail is fundamentally a leveraged business, there’s very little room for changing directions quickly since margins are so small. DG has hit a snag trying to build out stores in some of the better markets and I have at least three reports of better capitalized retailers outbidding them on sites. They’ve topped and are at the end of their boom cycle, not the beginning.

Dollar Tree (8) We’re up a respectable 7% on DLTR but this is a long-term bet, not short-term trade. This is another discounter that has had three consecutive years of double-digit stock price growth (2010- 74%, 2011- 47%, 2012 YTD- about 23%). DLTR and its ilk were short term plays on the consumer trading down, not a long-term place for your money.

MS (8) Something is going on with Morgan Stanley, I’m hearing more and more anecdotes about long-term clients in investment banking and trading counterparties fleeing. Plus the showdown with Citigroup over the valuation of Smith Barney is scaring wealth management clients. My analyst in the CDS market informs me that there are ever more sovereign wealth funds hedging their exposure to Morgan Stanley. The earnings call was terrible, their revenue from trading is going away and they risked more of their capital and made less on it than any other big bank.

JPM (7) The Dimon halo is gone, Chase’s retail footprint just can’t grow any more, and that juicy overdraft revenue is disappearing. Plus JPM can talk all it wants about Europe not hurting the balance sheet but it is plenty levered to plenty of slowing EU economies. Prop trading income will decline next year and there’s a big mortgage modification lawsuit sitting out there, all the pieces to make JPM a great short set up.

PSO (7) Pearson is in a storm of European revenues being crimped just as U.S. revenues are about to decline. Their testing business is looking particularly weak as fewer students can afford grad school entrance exams. The fall is going to be a critical time for our short as the testing scandal comes back, parents haven’t forgotten that Pearson made their kids sit in exams for an extra two hours to help their bottom line. And the publishing business is going to start seeing double digit declines in revenue soon, which the ebook business just won’t be able to make up.

LPS (8) The LIBOR and EU-crisis have put the putback fraud on the backburner but LPS is definitely not out of the woods. The big settlement gift that the banks got means that foreclosures are going to be ramping again. And that process is really expensive for LPS to handle, they have to service to paper for a long time, every call they make and every letter they send saps margins. In states where people can actually litigate their house being taken the process can take forever; New Jersey is at an average of 600 days. Big storm clouds await.