Will 2024 Be Rocket Lab’s Inflection Year? Our Updated Model (And Two Trade Alerts)

We will do chat at the regular time this week (Wednesday, January 4th at 3:00pm ET) in the TradingWithCody.com chat room or send your questions via email to support@tradingwithcody.com.

Also, please Follow us on our LinkedIn Page and Connect and Follow Cody here.

As promised, I’ve had Bryce update our Rocket Lab models and we’ve done a complete review and update to our analysis on it here. Here’s what Bryce put together from the updates and review. I will hop back on at the end of his detailed analysis below.

Also, we are selling Globalstar (GSAT) over the next few days. There are too many questions around the value of the company’s spectrum assets and we are a little uncomfortable with the valuation at this moment (stock is trading at 10x 2023 sales). Further, we are growing more confident in the T-Mobile (TMUS)/SpaceX sat-to-cell strategy which does not rely on new and unproven spectrum band usage. We started building a small position in TMUS accordingly and plan to buy it more aggressively if/when we get a pullback in the stock. We’ll have more analysis and details on this new position soon.

Now onto today’s piece…

Following Rocket Lab’s historic $515 million government contract award last month and on again/off again launch schedule in the last quarter of 2023, we wanted to update our model and reassess our bullish case for the company. Despite the pop in 2023, the stock is still down nearly 50% from its de-SPAC price ($10) where we were originally buying it. Thus, we thought it was time to dive deep into the company’s business model to figure out if this is a stock that we want to stick with for 2024.

As discussed below, we have some worries about Rocket Lab’s launch business, but we think this new government contract could be a game changer for the company and it’s exactly these types of contracts from governments that can only be awarded to about three companies right now (SpaceX, Rocket Lab and maybe Blue Origin). More than anything, it de-risks the company significantly and opens the door to new major satellite customers that Rocket Lab probably would not have been signed with Rocket lab without this major stamp of approval from the government. Without further ado, let’s get into it.

2023 In Review

Let’s start by quickly looking back. For Rocket Lab, 2023 turned out to be a rather lackluster year. The company only completed 10 successful Electron launches, 33% less than its originally-predicted 15 launches for 2023. This miss was the result of a slower launch cadence resulting from a rocket failure that occurred in September and effectively pushed the remainder of the year’s launch manifest into 2024. Further, Rocket Lab’s space-systems division — which produces satellites, satellite components, and associated software — only grew about 12% year over year (assuming the fourth quarter comes in line with company estimates). That’s less than stellar growth for a division of a company that trades at 10x sales.

Despite these operational troubles, Rocket Lab’s stock had a relatively solid year, gaining 46.7%, with over half of that gain coming in December after the company reported the new contract. Amongst space stocks, Rocket Lab was one of the best-performing stocks of the year with most of its compatriots flat or down significantly (look at stocks like SPCE, ASTR, PL, LUNR, etc.). Others failed completely, including Rocket Lab’s direct competitor, Virgin Orbit (VORB) which filed for Chapter 11 bankruptcy protection in April. Considering this landscape, Rocket Lab’s stock had a great year. In fact, it was up even more than SpaceX’s valuation which climbed about 31% in 2023 to $180 billion.

Updated Model

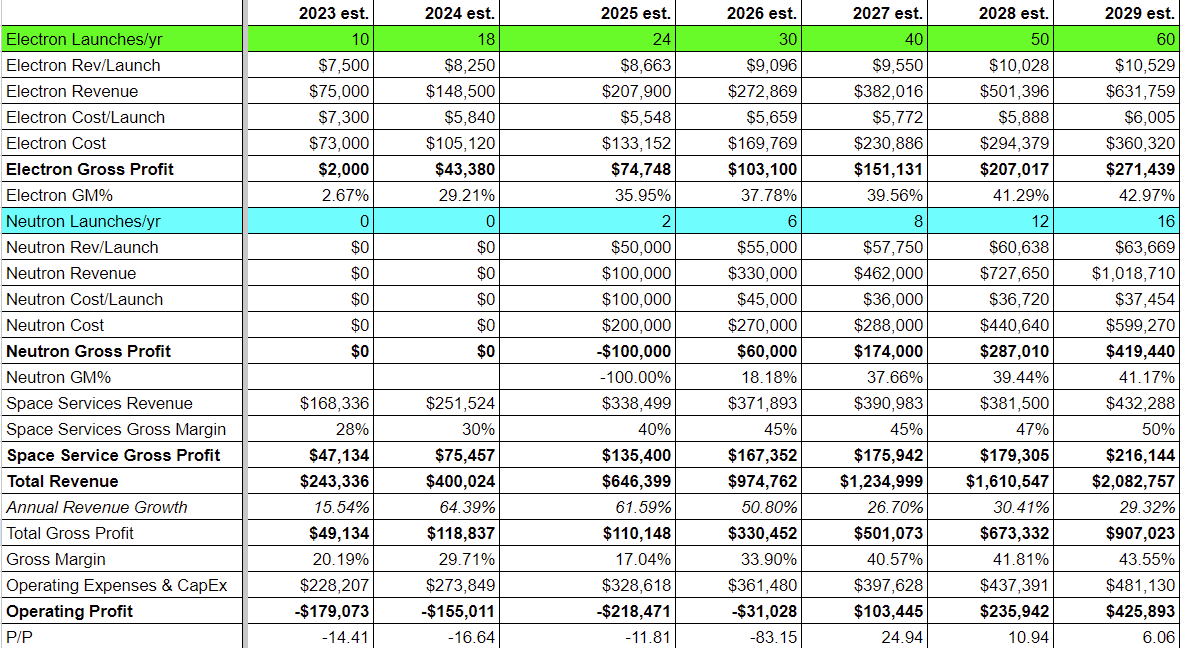

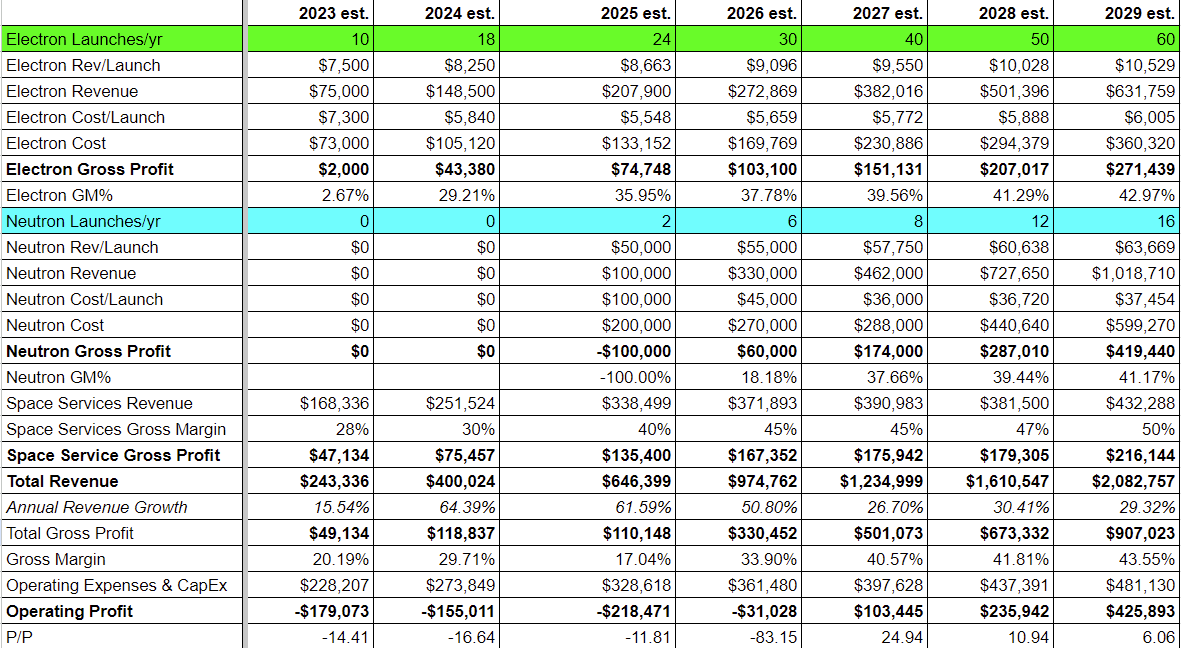

Rocket Lab is currently valued at about $2.5 billion, is estimated to have $250 million in sales in 2023, is not yet profitable, and is still burning lots of cash. Below is our model for Rocket Lab’s financials for the next five years. In addition to adding in new revenue growth resulting from the government contract, we took a hard look at Rocket Lab’s launch business, gross margins, operating expenses, etc., to generate what we hope is a realistic model. We’ll discuss all of the levers here in turn.

Electron

We’ll start with Electron, i.e., Rocket Lab’s existing launch business. Electron is a 59′ tall x 3.9′ diameter carbon composite rocket that is capable of hauling 661 lbs of mass to low-earth orbit (LEO). Rocket Lab’s customers use Electron to launch small satellites into LEO for communications, earth observation, and research purposes, among others. Within the “Electron” bucket we also include Rocket Lab’s recently created “HASTE” suborbital rocket, which is a slightly modified version of Electron that Rocket Lab designed to aid in hypersonic missile testing for the military.

Rocket Lab has thus far struggled to significantly increase the pace of its Electron launches. In 2022, the company completed 9 successful launches and expected to increase that number to 15 this year, but fell short when a launch for Capella Space failed in September and effectively placed the launch program on hold for the rest of the year. Rocket Lab’s Electron manifest is booked up for 2024 and the company is shooting for 22 launches this year, but we think 18 might be more realistic given the company’s struggles to increase cadence thus far.

Despite the failure to launch as many Electrons as planned, Rocket Lab made nice progress in improving Electron’s profitability of late. In the third quarter, Electron had GAAP gross margins of 27%. The company is realizing economies of scale as it attempts to increase launch cadence and we are encouraged by the improving margins. We model Electron costs decreasing 20% in 2024 in line with this trend and also expect pricing to improve as Rocket Lab is the only alternative to SpaceX for reliable launches to LEO right now. The company has reportedly worked through most of its older backlog that was fixed at lower launch prices and should be in a strong position to raise pricing for new contracts going forward.

In our view, 2024 will be a “show me” year for Electron. With Electron, Rocket Lab offers a (mostly) reliable option to get to LEO, but can it effectively scale? The company’s failure to meaningfully step up its launch cadence from 2022 levels is frustrating (it went from 9 to 10 launches last year). But space is hard and Rocket Lab has done a much better job than its competitors ex-SpaceX, so the company gets a pass for 2023. However, we think a second year of missed expectations could sour investor sentiment and put Rocket Lab in a precarious position if financial conditions are tighter than today at the end of the year. The company will likely burn through another $150 million or so in cash this year and might need to raise more money at some point in the next two years. The market will be much more apt to give Rocket Lab more money if it can show that its launch business is actually scaleable and not a glorified science project. That’s compared to SpaceX, which is expecting to launch 180 times this year, or once every other day.

Neutron

Neutron is Rocket Lab’s attempted answer to SpaceX. While still much smaller than SpaceX’s workhorse Falcon 9 rocket (which hauls 25 tons to LEO), Neutron will be much larger than anything else in the market coming in at 141′ tall with a 23′ diameter. The rocket will have the capability to carry over 14 tons of mass to LEO and is intended to be fully reusable.

Neutron is still in development and Rocket Lab is hoping to conduct the first test flight of the new rocket sometime in 2024. The company is testing and manufacturing its new Archimedes engine which will power Neutron and has also successfully tested the carbon composite fuel tank for its second-stage rocket.

We are hopeful to see a Neutron flight sometime this year but think it is not unlikely that the test slips into 2025. We currently model 2 commercial flights in 2025 with Neutron ramping slowly for the next few years. The company is expecting to charge $50 million per Neutron flight. This equates to about $3,800/kg which is quite a bit more than the present estimated Falcon 9 cost of $2,700/kg. The higher cost per kilo could present a challenge for Rocket Lab as it looks to fill up Neutron’s manifest with major constellation customers like Amazon, the EU, and the over 300 other planned constellation operators that will need a lift into LEO. With only two companies on the planet offering launches to LEO, there’s probably plenty of demand for Neutron’s launch capacity even at the higher price than SpaceX which is backlogged for years.

Neutron needs to work. For Rocket Lab to be a truly successful launch company, it needs to show that it can reliably and efficiently haul hundreds, if not thousands, of tons of mass to LEO and beyond. The small launch market that Rocket Lab currently serves is fine, but the cost/KG with Electron is very expensive compared to any of SpaceX’s current options, and perhaps an order of magnitude more expensive than when Starship is ready to go commercial (we expect that the price/KG could drop to a few hundred dollars with Starship). SpaceX isn’t slowing down, and if Rocket Lab cannot start to bring its costs/KG down significantly, it may start to lose customers to SpaceX in years ahead. The whole Space Revolution is premised on access to space becoming more and more affordable by orders of magnitude, thus enabling more and more applications, use cases, and research in space that otherwise would not take place. That won’t happen by launching 661 pounds into space at a time with rockets like Electron and Neutron is a big step in the necessary direction.

Space Systems

Rocket Lab’s space-systems division is a result of the acquisition of at least four separate companies: Sinclair Interplanetary (satellite manufacturer), Advanced Solutions (spacecraft software), Planetary Systems (spacecraft separation systems), SolAero Technologies (satellite solar panels). Together under Rocket Lab, these four companies now offer an end-to-end platform for customers looking for one firm to build, design, and operate satellites. Space-systems revenue made up 65% of Rocket Lab’s total revenue in the first nine months of 2023. The bulk of the revenue is coming from Rocket Lab’s $143 million contract with MDA Ltd. (MDA.TO) to build components for 17 satellites for Globalstar’s (GSAT) next-generation direct-to-cell constellation for Apple (AAPL).

The space-systems division grew rapidly in 2022 as Rocket Lab realized its first full year of revenue from its four acquired companies. However, if fourth-quarter revenues for the division are in line with management’s guidance, then this division will have only saw roughly 12% year-over-year revenue growth in 2023. That’s not very exciting, but…

Then, Christmas came early for Rocket Lab shareholders. On December 21, Rocket Lab told us that an undisclosed US government agency awarded it a contract valued at $515 million over the next six years. While the details are still sparse, the company indicated that it will build 18 spacecraft for the U.S. government with an expected launch in 2027. Rocket Lab will then “operate” the spacecraft through 2030 with an option to extend operations through 2033. The current speculation is that this contract is for the Space Development Agency (SDA) which is building out the Proliferated Warfighter Space Architecture (PWSA). The PWSA is a planned 90-satellite constellation that will enable next generation voice and other low-data communications for American military operations on the ground. Lockheed Martin (LMT) and Northrup Grumman (NOC) received a combined $1.5 billion in contracts from the SDA for the other 72 satellites in the PWSA earlier this year.

This is obviously a major deal for Rocket Lab and a major sign of validation in the company from the U.S. government. Here’s how we modeled the incremental revenue from the new contract (numbers are in the 1000s):

We model the bulk of the contract value (75% est.) is for the satellites themselves which will be realized through 2027 when the satellites will launch. We expect Rocket Lab will realize the remainder of the contract revenue (25% est.) in the last three years for the operation of the spacecraft.

We expect Rocket Lab’s existing space-systems revenue to continue to grow in the mid- teens, but with the new contract added in, we see total systems revenue growing close to 50% Y/Y in 2024 and nearly 35% in 2025. Gross margins for the division increased from 17% to 28% in 2023 and we expect those numbers to continue to climb as the various divisions become more integrated into the company and the company becomes more efficient accordingly. Especially considering Rocket Lab’s proprietary software offerings, we think gross margins for the system’s division can reach the 40% range within two years and potentially be closer to 50% in five years. This is very complicated and specialized work and we expect Rocket Lab will have growing pricing power for its space systems over time.

In sum, we think the new government contract could indeed be a game changer for Rocket Lab’s prospects over the new five years. If this contract turns out to be part of the SDA’s PWSA program, then it puts Rocket Lab’s satellite-manufacturing capabilities on par with major primes like Lockheed Martin and Northrup Grumman. This contract alone has us really excited about the space -systems division, and we think it opens the door to more major contracts for Rocket Lab over the next few years from the governments of the US and her allies, plus major commercial customers as well (more of the MDA/Globalstar/Apple-type deals).

Operating Expenses

Rocket Lab is expected to spend about $228 million on operating and capital expenses in 2023, up from $154 million in 2022. This is driven by heavy R&D costs for new rocket programs (HASTE and Neutron) as well as capex for building out new launch facilities in Virginia and rocket manufacturing facilities in California. We model expenses growing by 20% for the next two years, then leveling out at 10% growth thereafter. Rocket Lab actually reduced operating expenses in the third quarter and we are fairly confident in CEO Peter Beck’s continued ability to run a lean ship. Ultimately, we think the company can achieve close to 20% operating margins.

Conclusion

Our updated model shows Rocket Lab growing revenue by 4x to a $1 billion run rate in three years and doubling again by 2029. Given the high mix of high-margin space-systems revenue, overall gross margins have the potential to approach the 40% level. We think the company has two more years of heavy spending to effectively scale Electron and bring Neutron to life, but should demonstrate substantial operating leverage as the high-fixed-cost nature of the launch business starts to get spread out over a rapidly increasing launch cadence.

As always, there is still major risk involved with owning a small-cap stock like Rocket Lab. For one, there is clearly risks to the downside if 2024 turns out to be another 2023 with the launch business. The company could also suffer another launch failure like it did this September. Moreover, the company is still burning cash and will continue to do so for the next two years most likely.

However, we think the $515 million contract has helped de-risk the stock. Even if the launch business continues to struggle in the near term, we think there is room to the upside given the potential for Rocket Lab to sign more major contracts for satellite manufacturing and operation. Historically, many of Rocket Lab’s more notable satellite customers ended up launching with SpaceX because the satellites were too big for Rocket Lab to haul with Electron. Thus, there is a viable path forward for the biggest part of Rocket Lab’s business to continue to grow rapidly with or without Neutron coming online soon.

With the stock trading at a 6 price/profits (P/P) ratio 5 years out, we like the risk/reward setup for Rocket Lab right here. We are not chasing the stock but we might look to add to our currently medium-sized position if the stock gets back around or below $5.

Cody back again now. Space is famously hard. But The Space Revolution is on pace to change the world (solar system) in coming years and Rocket Lab is one of a very few space companies that are currently trading in the public markets that has a real chance to be one of the big winners if they execute well enough. As always, be careful and manage carefully how much risk you take with a still unprofitable smaller cap company like this.

To the moon, as they say — at least that’s one of the near-term goals for those in the space industry. Haha. See you tomorrow at the chat.